Rising Rents, Falling Rates: What This Means for Yields

As mortgage rates ease and rental demand stays strong, landlords across the UK are finally seeing relief on yields. Here’s what the changing rate landscape means for property investors — and why SPV ownership continues to rise.

The Market Is Finally Balancing Out

After two years of turbulence, 2025 has shaped up to be a turning point for UK property investors.

The Bank of England’s gradual rate cuts have started to feed through into buy-to-let mortgage pricing, while tenant demand, fuelled by continuous limited housing supply remains incredibly strong.

The result? Rising rents, falling rates, and healthier yields.

But that’s only half the story. How you own your properties, either personally or through a limited company (SPV) could make the biggest difference to your long-term returns. Also, looking at other property options such as HMO’s, Semi'-commercial, Multi-unit freehold blocks, Holiday lets and so much more could spread your risk and create further opportunity with your capital. Have a look in more detail at the opportunities in our Investor Hub.

Rental Growth: The Backbone of Yields

Rental inflation has persisted across most regions, especially Manchester, Liverpool, and Leeds, where young professionals and students compete fiercely for quality accommodation.

According to the latest data, average rents in the North West rose by around 6–8% year-on-year. Combined with more affordable mortgage products now returning to the market, investors are enjoying yield margins they haven’t seen since 2021.

Why It Matters

Gross yields are improving, meaning better cash flow.

Void periods are falling - strong demand keeps properties occupied.

Tenants are staying longer, providing more predictable income streams.

For investors focused on income rather than rapid capital growth, 2026 could be one of the best windows to strengthen portfolio performance.

Falling Rates: Breathing Room for Investors

The peak in base rate appears to be behind us. As lenders adjust, several have reduced limited company buy-to-let rates by up to 1% since the start of the year.

The Impact

Lower monthly payments directly improve net yield.

Remortgaging opportunities are returning, particularly for landlords who fixed at higher rates in 2023–24.

Investors using interest-only SPV mortgages are seeing margins widen again.

stress tests are helping investors extract further funds.

For many, this renewed affordability is allowing expansion that was paused during the high-rate environment.

Why More Landlords Are Moving into SPVs

1. Tax Efficiency

When you own properties through a Special Purpose Vehicle (SPV), mortgage interest can be offset as a business expense - something no longer available to individual landlords. This single difference can transform a property from loss-making to profitable.

2. Simplified Reinvestment

Profits earned in the company can be reinvested into new acquisitions without drawing dividends or incurring personal tax. That allows your portfolio to grow faster, using retained profits as deposits.

3. Lender Appetite

SPV lending has exploded in recent years. Specialist lenders now dominate this space, offering flexible criteria and higher loan-to-value (LTV) products designed for professional landlords.

It’s no longer a niche strategy — it’s becoming the mainstream.

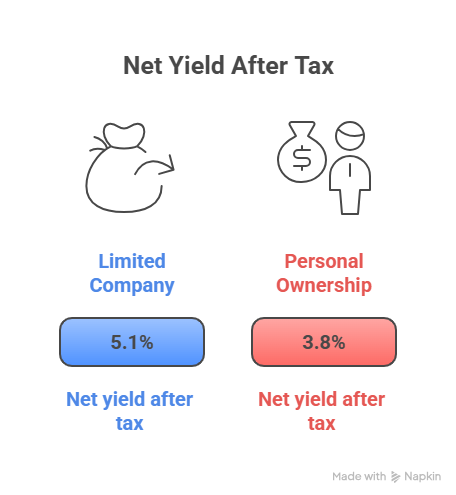

The Numbers in Action

Let’s take a simple example:

A landlord with a £250,000 property rented at £1,250 per month.

Personal ownership (basic-rate taxpayer): After mortgage interest and tax, net yield ≈ 3.8%.

Limited company ownership: After corporation tax and deductible interest, net yield ≈ 5.1%.

That 1.3% margin on a small portfolio adds up fast - and for higher-rate taxpayers, the difference can be even greater.

For more insights like this, visit our Investor Hub or contact us directly - Contact us

The Outlook for 2026

With interest rates cooling and rents remaining high, the fundamentals for UK property investors look strong. The limited company model not only enhances profitability but also offers more control over long-term planning; especially when considering inheritance or joint ventures.

Investors who can refinance strategically, reduce borrowing costs, and reinvest tax-efficiently are likely to outperform in this next phase of the cycle.

The big taking point going into November is the Autumn Budget and what this might mean for Landlords. you can read our insights here, or speak to us to discuss your options.

Our Take

We have seen more limited-company landlords enter the market this year. Whether you own two properties or twenty, the question isn’t just how high your yield is, it’s how efficiently you’re structured to keep it.

Next Steps

Thinking about incorporating your portfolio or refinancing into a limited company structure?

Book a free portfolio review with our team — we’ll walk you through the figures, lender options, and tax considerations before you act.

Manchester Independent Mortgages Ltd is authorised and regulated by the Financial Conduct Authority (FCA 431647). The information above is for guidance only and does not constitute personal advice. Your home may be repossessed if you do not keep up repayments on your mortgage.